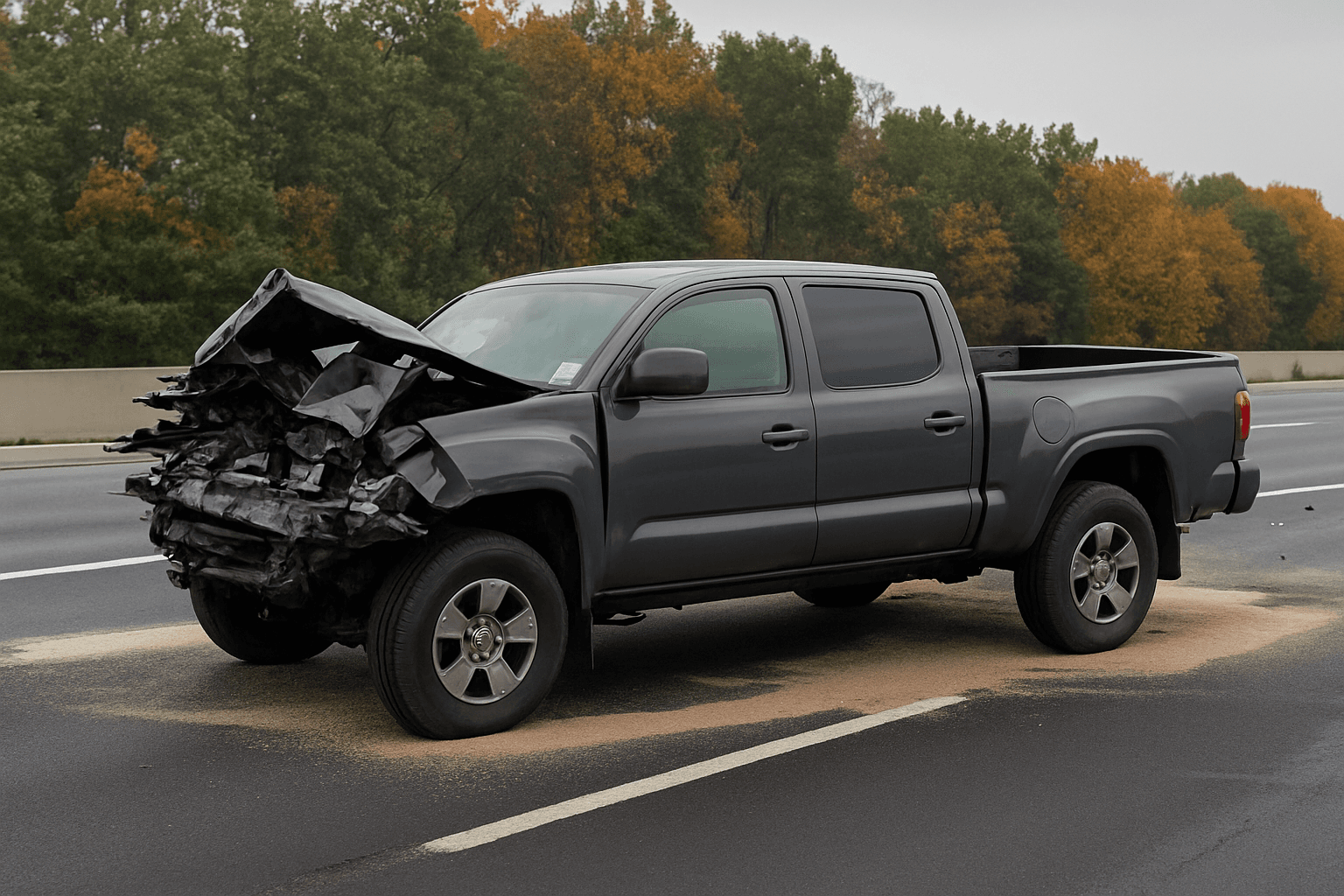

When you cause an accident that sends someone to the hospital, your insurance rates don't just go up — you face layered liability exposure, multi-year rate increases, and potential coverage cancellation. Here's what happens next and what you need to do before your renewal date.

What Happens to Your Insurance After an At-Fault Accident with Injuries

Your current policy will likely cover the immediate claim, but three separate consequences start the moment the accident report lists injuries. First, your liability coverage pays medical bills, lost wages, and pain and suffering claims up to your policy limits — if the injured party's damages exceed those limits, they can pursue your personal assets through a lawsuit. Second, your rate increase takes effect at your next renewal date, not immediately — most drivers don't see the premium jump for 30 to 90 days after the accident. Third, your carrier evaluates whether to renew your policy at all, and many standard carriers non-renew drivers after a single at-fault accident involving injuries, especially if your record already includes a prior claim or violation.

The rate increase itself is not a flat percentage. Carriers apply a surcharge based on the severity of the accident, measured by total payout and injury type. An accident with $15,000 in medical claims typically increases your premium by 40 to 60 percent. An accident with $50,000 or more in claims can double your rate or push you into non-standard coverage entirely. These increases compound if you carry minimum liability limits, because carriers view low-limit policies as higher risk after a serious claim.

Non-renewal is the outcome most drivers miss until the notice arrives. Standard carriers — State Farm, Allstate, Farmers, Liberty Mutual — typically allow one at-fault accident before non-renewing, but if injuries are involved or if the payout crosses a certain threshold, that tolerance drops to zero. You will receive a non-renewal notice 30 to 60 days before your policy ends, depending on your state. That notice does not cancel your current coverage, but it means you must find a new carrier before the end date or enter a coverage gap, which triggers license suspension in most states and makes finding any coverage significantly harder.

How Liability Limits Work When Injuries Exceed Your Coverage

Liability coverage is expressed as three numbers: bodily injury per person, bodily injury per accident, and property damage. A common minimum-limit policy is 25/50/25, meaning your insurer pays up to $25,000 per injured person, $50,000 total per accident for all injuries, and $25,000 for property damage. If one person's medical bills, lost income, and settlement demand total $80,000, your policy pays the first $25,000, and you are personally liable for the remaining $55,000.

The injured party can file a lawsuit to recover that difference. If they win a judgment, they can pursue wage garnishment, bank account liens, or forced sale of non-exempt assets depending on your state's creditor protection laws. Some states protect your primary residence and retirement accounts; most do not protect cash savings, investment accounts, or secondary property. Liability beyond policy limits is not theoretical — it is the most common financial consequence of an at-fault accident with serious injuries, and it is why umbrella policies exist.

If you carry higher limits — 100/300/100 or 250/500/100 — your exposure shrinks significantly. A $100,000-per-person limit covers most single-injury claims without reaching your personal assets. Umbrella coverage adds another $1 million to $2 million on top of your auto liability limits for $150 to $300 per year. After an at-fault injury accident, your ability to buy umbrella coverage ends until the claim closes and the rate increase period expires, which is why increasing liability limits or adding umbrella coverage before an accident is the only window most drivers have.

Find out exactly how long SR-22 is required in your state

The Rate Increase Timeline and How Long It Lasts

Your rate does not increase the day after the accident. The increase appears at your next renewal date, which could be 30 days or 11 months away depending on when the accident occurred in your policy term. If your renewal date is May 1 and the accident happens on May 15, you will not see the rate change until the following May 1 renewal. During that period, your current premium stays the same, but your carrier is processing the claim and determining your surcharge.

The surcharge itself lasts for 3 to 5 years from the renewal date, not from the accident date. Most states allow carriers to surcharge an at-fault accident for three years; some states extend that to five years for accidents involving injuries or high payouts. California limits the surcharge period to three years by law. Texas allows five years. The surcharge does not decrease gradually — it applies in full for the entire period, then drops off completely at the end.

If you switch carriers during the surcharge period, the new carrier will see the accident on your motor vehicle report and apply their own surcharge, which may be higher or lower than your current carrier's rate. Shopping your rate annually during the surcharge period is one of the few ways to reduce the total cost, because non-standard carriers price at-fault accidents differently. Progressive may surcharge 50 percent while Dairyland surcharges 70 percent for the same accident, and both are quoting the same driver with the same record.

What Non-Renewal Means and Where to Find Coverage Next

Non-renewal is not the same as cancellation. Your current policy remains active until the end of the term listed in the non-renewal notice, and your carrier continues to cover claims that occur before that end date. The notice simply means they will not offer you another term. You are not being dropped mid-policy unless you stop paying premiums or commit fraud.

Most drivers who receive a non-renewal notice after an at-fault injury accident move into the non-standard insurance market. Non-standard carriers specialize in high-risk drivers — those with at-fault accidents, DUIs, license suspensions, or lapses on their record. The coverage itself is identical to standard insurance; what differs is the carrier's willingness to write drivers that State Farm or Allstate declined. Common non-standard carriers include Progressive, Dairyland, The General, Bristol West, National General, Acceptance Insurance, and SafeAuto.

Non-standard premiums are higher than standard premiums, but not always by the margin most drivers expect. A driver paying $140 per month with a standard carrier before the accident might pay $210 to $280 per month with a non-standard carrier after non-renewal, depending on the state, the total claim payout, and the driver's age. Drivers under 25 or over 65 typically see steeper increases. The key is shopping multiple non-standard carriers, because rate variation in this market is extreme — one carrier may quote $320 per month while another quotes $215 for identical coverage.

You can begin shopping for non-standard coverage the day you receive the non-renewal notice. You do not need to wait until your current policy ends. Most drivers benefit from securing a new policy 15 to 30 days before the non-renewal date to avoid any gap in coverage, which would appear on your record and trigger a lapse surcharge on top of the accident surcharge.

Whether You Need an Attorney and When to Hire One

If the injured party's medical bills are approaching or exceeding your liability limits, you need an attorney before the claim becomes a lawsuit. Your insurance company provides a defense attorney if a lawsuit is filed, but that attorney represents the insurer's interests, not yours. If your policy limit is $25,000 and the claim demand is $80,000, the insurer's goal is to settle within the $25,000 limit and close the file. Your goal is to protect your personal assets from the $55,000 difference.

A personal injury defense attorney evaluates the claim, determines whether the demand is reasonable, negotiates directly with the injured party's attorney, and structures settlement agreements that protect your assets. In some cases, they negotiate payment plans or reduced settlements that avoid wage garnishment or asset liens. Legal fees for this work typically range from $2,500 to $7,500 depending on case complexity and whether the case goes to trial.

You should consult an attorney if: the injured party hires a lawyer, your insurer sends you a letter stating that the claim may exceed your policy limits (called an excess letter), or the total medical bills already exceed 75 percent of your per-person liability limit. Waiting until a judgment is filed eliminates most negotiating leverage. Early consultation — within 60 days of the accident — preserves options that disappear once the legal process advances.

What to Do Right Now

These steps apply whether you received the non-renewal notice yesterday or you are still waiting to hear from your carrier.

1. Request a copy of the accident report and the claim file from your insurer within 10 days of the accident. The accident report shows whether the other party reported injuries at the scene, which triggers the liability and rate consequences described above. The claim file shows the current payout estimate and whether your insurer believes the claim will exceed your limits. If you wait until the non-renewal notice arrives, you have already lost 30 to 90 days of decision-making time.

2. Confirm your policy renewal date and mark the non-renewal deadline if you receive a notice. Non-renewal notices include a specific end date, typically 30 to 60 days from the notice date depending on state law. Missing that date by even one day creates a coverage gap, which appears on your motor vehicle report and adds a lapse surcharge to your already-elevated premium. Set a calendar reminder for 15 days before the deadline to begin securing new coverage.

3. Get quotes from at least three non-standard carriers before your current policy ends. Standard carriers will decline you or quote premiums 80 to 120 percent higher than non-standard specialists. Progressive, Dairyland, The General, and Bristol West all write drivers with recent at-fault accidents involving injuries. Rate variation between non-standard carriers often exceeds $100 per month for identical coverage, so a single quote leaves money on the table.

4. If the claim estimate exceeds 75 percent of your liability limit, consult a personal injury defense attorney within 60 days of the accident. Waiting until a lawsuit is filed eliminates most settlement options and exposes your assets to judgment liens. Early consultation costs $200 to $500 for an initial review and preserves negotiating leverage that disappears once the injured party's attorney files in court. If you cannot afford an attorney, some state bar associations offer reduced-fee referral programs for drivers facing excess liability claims.

5. Do not let your coverage lapse between your current policy end date and your new policy start date. Even a single day of no coverage triggers a lapse notation on your record, which compounds your rate increase and can result in license suspension in most states. Schedule your new policy to begin the day after your current policy ends, and confirm the start date in writing with the new carrier.