You hit a guardrail, rolled into a ditch, or slid off the road with no other vehicle involved. Your insurer still knows, and your rates are about to change. Here's what happens next and how single-vehicle at-fault accidents affect your premium.

What Your Insurer Sees When You File a Single-Vehicle Claim

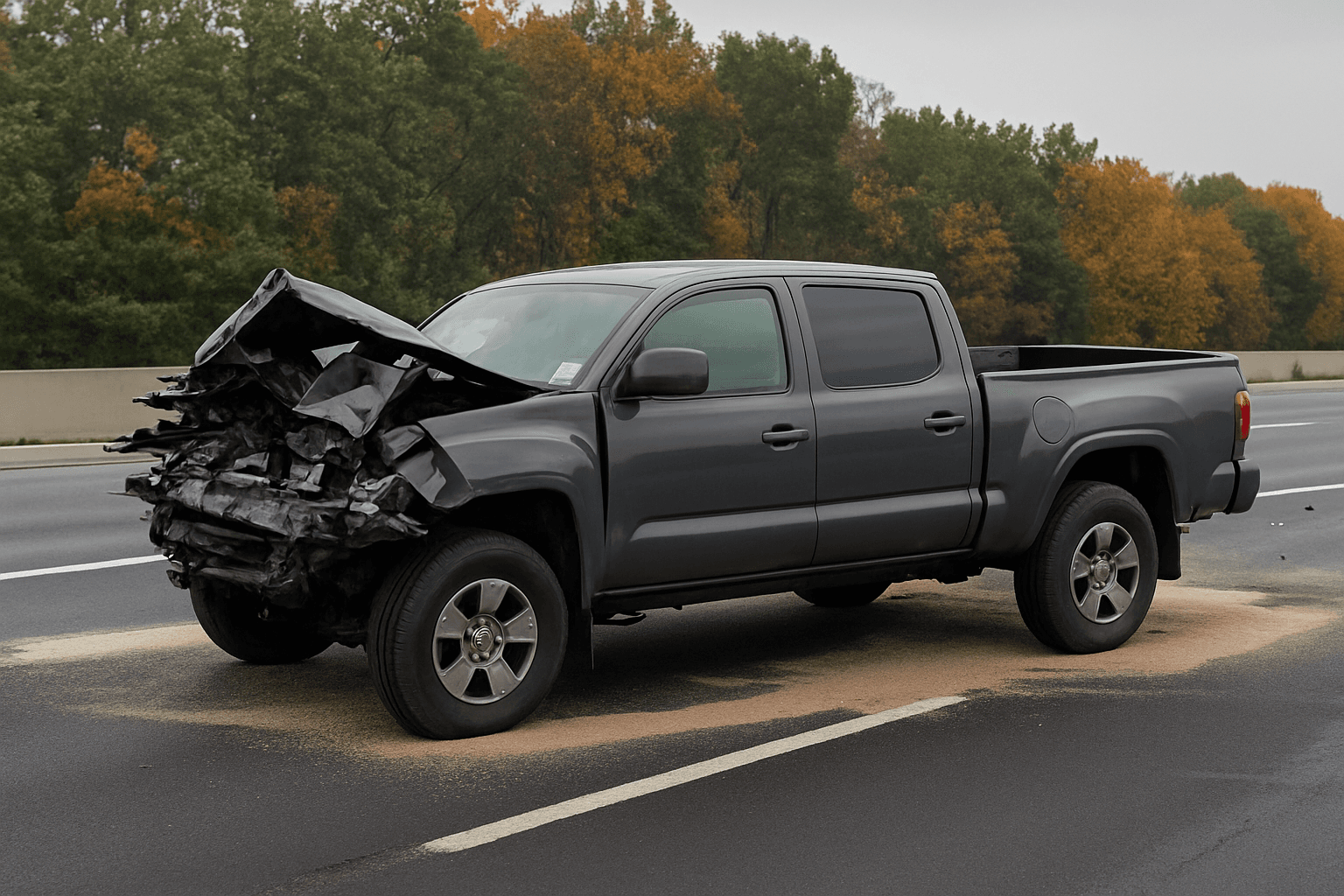

A single-vehicle at-fault accident — hitting a tree, guardrail, mailbox, or rolling your car in a ditch — tells your insurance carrier one thing: you were the sole cause. There's no other driver to share fault with, no dispute over who merged into whom, no ambiguity.

From the carrier's perspective, this is a clean data point. You lost control of your vehicle, and the loss happened entirely under your operation. That clarity makes single-vehicle accidents highly predictive of future claims in actuarial models, which is why they trigger rate increases even when the damage is minor.

Your carrier learns about the accident the moment you file a claim for your own vehicle damage under collision coverage. Even if you don't file a claim, a police report filed at the scene typically flows into the LexisNexis or Verisk databases that insurers check at renewal. If the accident involved a citation for careless driving, failure to maintain control, or DUI, the rate impact compounds.

How Much Your Rate Will Increase After a Single-Vehicle At-Fault Accident

Expect a rate increase of 20% to 50% at your next renewal, depending on your state, your carrier, and your driving history before the accident. Drivers with clean records typically see increases on the lower end of that range. Drivers with prior violations or claims move toward the upper end.

In states like California and Massachusetts, insurers face restrictions on how much they can increase rates after a first at-fault accident, particularly if no injuries occurred. In states with fewer rate regulation constraints — Texas, Georgia, Florida — carriers price accidents more aggressively. The same single-vehicle rollover might add $300 annually in one state and $900 in another.

The increase appears at your renewal date, not immediately. Your current policy period runs out at the original rate. The new rate reflects the accident once your carrier recalculates your risk profile for the next six or twelve months. Most carriers apply the surcharge for three to five years, though the percentage impact typically decreases each year if no new incidents occur.

Find out exactly how long SR-22 is required in your state

Why Single-Vehicle Accidents Sometimes Hit Harder Than Two-Car Crashes

In a two-vehicle accident, fault is often split or contested. You might be found 30% at fault, or liability might shift entirely to the other driver after investigation. Insurers adjust premiums based on your assigned percentage of fault, and partial fault means a smaller surcharge.

Single-vehicle accidents eliminate that variable. You are 100% at fault by definition. The carrier has no reason to discount the surcharge, no claims adjuster from another insurer arguing their driver was responsible, no police report showing the other party ran a red light.

This is why hitting a deer — typically classified as a comprehensive claim, not collision — does not raise your rate the same way. Comprehensive claims reflect random events outside your control. Single-vehicle collisions reflect control failures, and carriers price them accordingly.

What Happens If You Don't File a Claim

Skipping the claim doesn't always hide the accident. If law enforcement responded, the incident generates a report. That report enters the databases insurers check when calculating your renewal premium, even if you never contacted your carrier.

In most states, police reports from accidents involving injuries, suspected impairment, or property damage above a threshold — typically $1,000 to $2,500 — must be filed with the DMV or state Department of Transportation. Those filings flow to LexisNexis and similar data aggregators within weeks. Your insurer pulls that report at renewal and applies the surcharge whether you filed a claim or not.

If the accident was minor, no police were called, and you paid out of pocket for repairs, your insurer likely won't learn about it unless you tell them. Choosing not to file a claim on a $1,200 fender repair might save you three years of rate increases that would total far more than the repair cost. Run the math before you file.

How Long the Accident Stays on Your Record

Single-vehicle at-fault accidents remain on your insurance record for three to five years in most states. The surcharge applied to your premium typically lasts the same duration, though the percentage impact often tapers after the first renewal cycle.

Your motor vehicle record (MVR) may show the accident longer if a citation was issued. A careless driving ticket or failure to maintain lane violation can stay visible for three years in some states, six in others. Insurers look at both your claims history and your MVR when pricing your policy, so the accident affects your rate until it ages off both records.

After the lookback period expires, the accident no longer factors into your quoted premium. You return to the rate tier you qualified for before the incident, assuming no new claims or violations appear in the interim.

If the Accident Involved a Violation or Substance Charge

A single-vehicle accident combined with a DUI, reckless driving, or suspended license charge moves you into high-risk or non-standard insurance territory immediately. Standard carriers either non-renew your policy at the next cycle or raise your rate to a point where switching becomes necessary.

High-risk auto insurance is not a different product. It's the same liability, collision, and comprehensive coverage sold by carriers that specialize in drivers with violations, DUIs, or serious accidents on record. Companies like Progressive, Dairyland, The General, and Bristol West write policies for drivers standard carriers decline.

If your state requires SR-22 filing after the violation, you'll need a carrier that offers SR-22 certificates. SR-22 is not insurance — it's a form your insurer files with the state proving you carry the required minimum coverage. Not all carriers file SR-22, which is why drivers in this situation often need to switch even if their current insurer doesn't cancel them outright.

What To Do Right Now

Step 1: Confirm whether a police report was filed. Contact the law enforcement agency that responded. If a report exists, request a copy. That report determines whether the accident will appear in insurance databases regardless of whether you filed a claim. Do this within two weeks of the accident.

Step 2: Calculate whether filing a claim makes financial sense. Add up three years of the expected rate increase based on your current premium and the 20-50% range. If that total exceeds your out-of-pocket repair cost by a significant margin, paying for repairs yourself avoids the surcharge. If you've already filed the claim, this step doesn't apply.

Step 3: Request a rating worksheet from your insurer at renewal. When your renewal notice arrives, call and ask for a breakdown showing how the accident affected your premium. Some states require insurers to provide this on request. Knowing the exact surcharge amount helps you comparison shop accurately.

Step 4: Compare quotes from high-risk carriers if your rate doubles or your policy is non-renewed. If your premium increases more than 60%, or if your carrier sends a non-renewal notice, get quotes from non-standard carriers within 30 days. Letting your policy lapse creates a coverage gap, which adds another surcharge on top of the accident when you re-enter the market. If your state requires SR-22 after the accident, confirm the new carrier offers SR-22 filing before you switch.