Michigan's no-fault insurance system treats first at-fault accidents differently than most states — your rate will increase, but you may avoid a surcharge if you stay with your current carrier and no one was injured.

What Just Happened to Your Insurance After This Accident

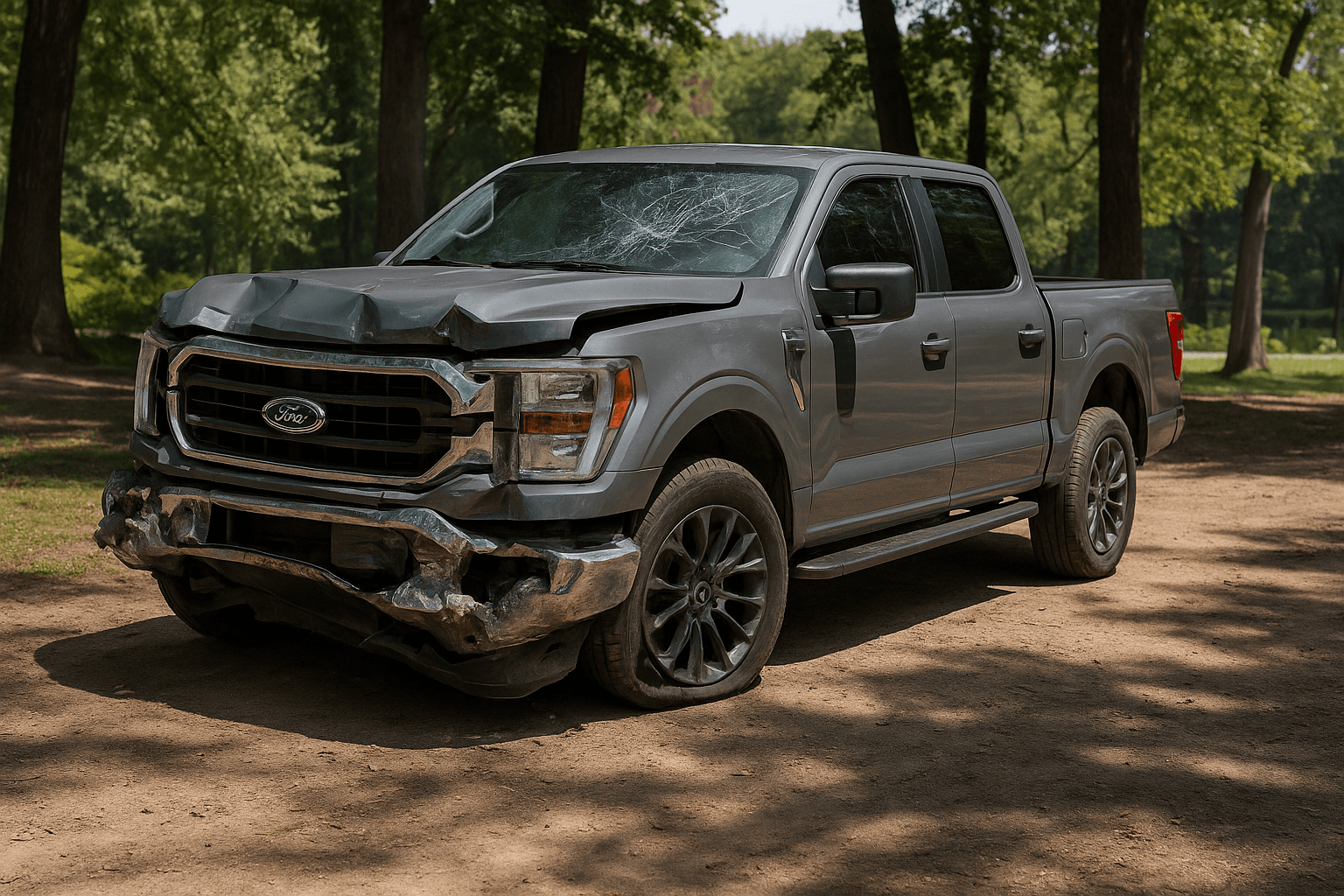

Your carrier now has an at-fault accident on your record. In Michigan, this triggers a rate increase at your next renewal — typically 20 to 40 percent for a first accident with no injuries. The increase applies even though Michigan's no-fault system means your own PIP coverage paid your medical bills, not the other driver's carrier.

Most standard carriers in Michigan keep first-time at-fault drivers in the standard risk pool if the accident involved property damage only and you have no other violations. If the accident caused injuries or totaled multiple vehicles, expect a steeper increase — 50 to 70 percent — and a higher chance your carrier will non-renew you at the end of your policy term.

The timing matters. Your current rate stays in effect until your policy renews. That gives you 30 to 180 days depending on where you are in your policy term to compare rates, understand what your current carrier will charge, and decide whether switching now saves you money or locks in a worse rate elsewhere.

How Michigan's No-Fault System Affects Your Rate After an At-Fault Accident

Michigan operates under a no-fault insurance system. This means your own Personal Injury Protection coverage pays your medical bills after any accident, regardless of who caused it. The other driver's carrier does not pay your hospital bills, and your carrier does not pay theirs — each driver's PIP handles their own medical costs.

Fault still matters for property damage and rate increases. If you caused the accident, you are listed as at-fault in your carrier's claims database. Your carrier paid out a collision claim to repair your car and a property damage liability claim to repair the other driver's car. Both claims count against your record.

This is different from tort states, where an at-fault accident means the other driver's carrier paid everything and your carrier only sees a liability payout. In Michigan, your carrier sees both the collision payout and the liability payout, but your PIP claim history — how much your medical coverage has paid over time — also factors into your rate. A driver with one at-fault accident and zero PIP claims typically sees a smaller increase than a driver with one at-fault accident and $40,000 in PIP payouts from prior accidents.

Find out exactly how long SR-22 is required in your state

What Your Rate Increase Will Look Like

A first at-fault accident in Michigan increases your premium by 20 to 40 percent on average if no injuries occurred and the total payout was under $10,000. If the accident caused injuries or your carrier paid out more than $25,000 combined across collision, property damage liability, and PIP, expect 50 to 70 percent.

Here's what that looks like in monthly premium terms. A driver paying $180 per month before the accident will pay $215 to $250 per month after a minor at-fault accident, or $270 to $305 per month after a serious one. Estimates based on available industry data; individual rates vary by driving history, vehicle, coverage selections, and location.

The increase stays on your record for three years in Michigan. After three years without another accident or violation, the surcharge drops off and your rate returns to the base tier. Some carriers reduce the surcharge incrementally each year — you might see the full increase in year one, 75 percent of it in year two, 50 percent in year three, then removal in year four.

Whether You Need to Switch Carriers or Can Stay Where You Are

Most standard carriers in Michigan — State Farm, Auto-Owners, Progressive, Allstate — will keep you after a first at-fault accident if your record was clean before and the accident did not involve serious injuries. You will pay more, but you stay in the standard risk pool.

If your carrier non-renews you, you will receive a notice 30 to 60 days before your policy term ends. Non-renewal is more common if the accident caused injuries, if you filed a PIP claim over $50,000, or if you have another violation within the past three years. Non-renewal does not mean you are uninsurable — it means your current carrier will not offer you another term at any price.

If you are non-renewed, you will need coverage from a carrier that writes higher-risk drivers. In Michigan, this typically means Dairyland, The General, National General, or Bristol West. These carriers charge 30 to 60 percent more than standard carriers for identical coverage, but they will write you a policy where standard carriers will not. Switching to a non-standard carrier before you are non-renewed does not save money unless their quote beats your current carrier's renewal rate after the surcharge.

How Long This Affects Your Insurance and When Rates Drop

The at-fault accident stays on your Michigan driving record and your carrier's claims history for three years from the accident date. Your rate increase applies for the full three years unless your carrier uses a step-down surcharge schedule.

After three years, the accident drops off and your rate returns to the base level for your age, vehicle, and coverage tier — assuming no new accidents or violations. If you switch carriers during the three-year window, the new carrier will see the at-fault accident during underwriting and apply their own surcharge. You cannot reset the clock by switching.

Some drivers see their rate drop before the three-year mark if they add another vehicle, move to a lower-risk ZIP code, or increase their deductible. These changes affect your base rate, not the accident surcharge, but the combined effect can lower your monthly premium even while the surcharge is still active.

What Happens If You Have Another Accident Before the Three Years End

A second at-fault accident within three years of the first moves you into high-risk or non-standard territory with most Michigan carriers. State Farm and Auto-Owners typically non-renew drivers after two at-fault accidents in a three-year window. Progressive and Allstate may keep you but will reclassify you into a higher-risk tier with rates 70 to 120 percent above your original premium.

If you are non-renewed after a second accident, expect to move to a non-standard carrier and pay $200 to $400 per month for state minimum liability coverage, depending on your age and location. Full coverage with collision and comprehensive will run $350 to $600 per month. These figures reflect current non-standard market pricing in Michigan; individual rates vary.

The three-year clock on each accident runs independently. If your first accident occurred in January 2024 and your second in June 2025, the first drops off in January 2027 and the second drops off in June 2028. Until both are off your record, you remain in the high-risk pool.

What To Do Right Now

Step 1: Contact your current carrier within 7 days of the accident and ask for a renewal quote reflecting the at-fault surcharge. Get this in writing. If you wait until your renewal notice arrives, you lose the comparison window and may face a coverage gap if you need to switch.

Step 2: Compare that renewal quote against quotes from at least two other standard carriers and one non-standard carrier. Run quotes for your current coverage limits and for Michigan state minimums. Some drivers save money by staying with their current carrier and raising their deductible rather than switching to a cheaper carrier with worse claims service.

Step 3: If your current carrier is non-renewing you, secure a new policy before your current term ends. A single day without coverage after an at-fault accident creates a lapse on your record, which will increase your rate with the next carrier by another 10 to 20 percent on top of the accident surcharge. Most non-standard carriers in Michigan can bind a policy within 24 hours if you call directly.

Step 4: If you are staying with your current carrier, confirm your renewal date and ask whether they offer accident forgiveness or a step-down surcharge schedule. Some carriers reduce the surcharge after 12 months if you complete a defensive driving course — but you must ask for it and provide proof of completion before your first renewal after the accident.