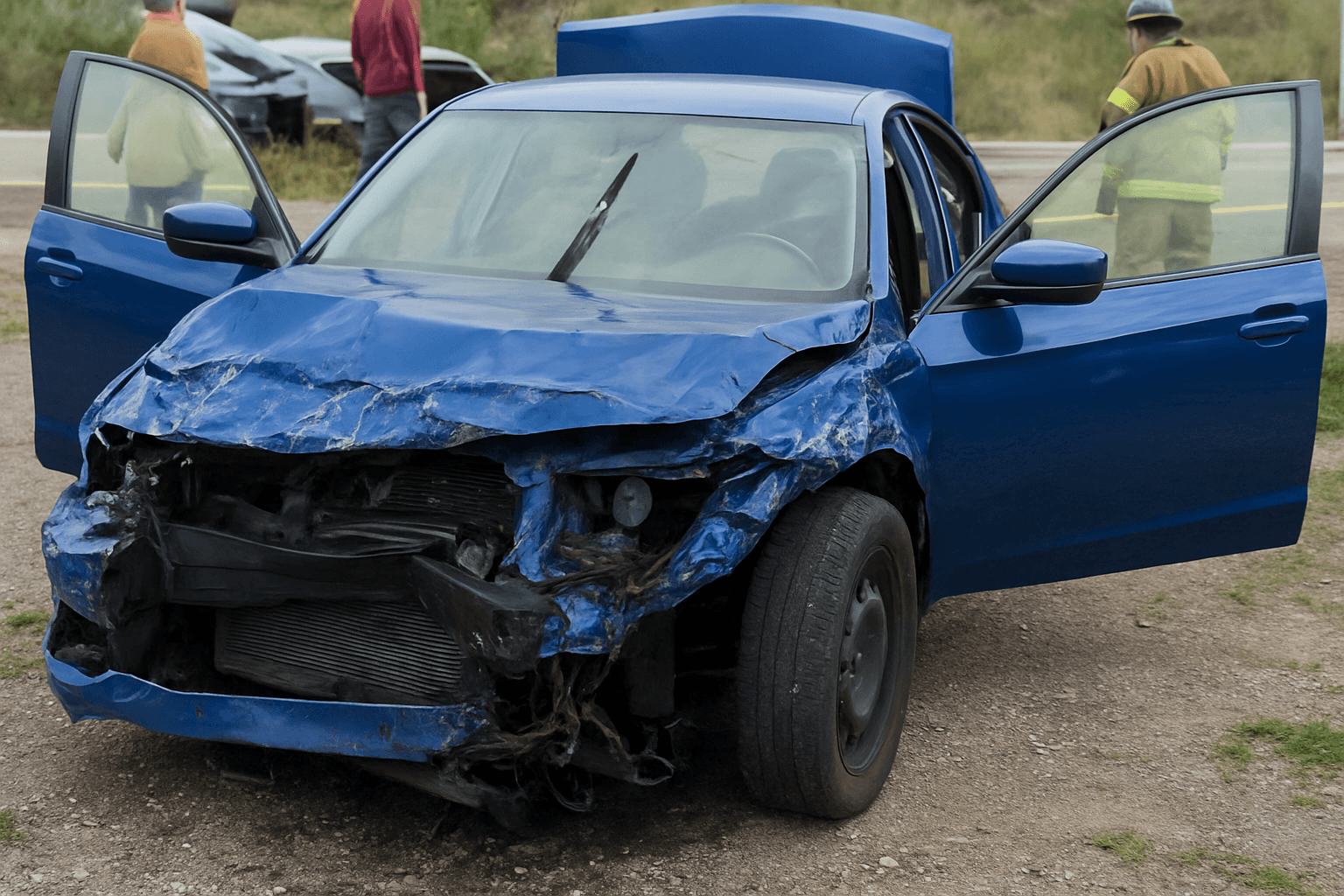

If you caused an accident without insurance, you face immediate financial liability for all damages plus state penalties that can escalate quickly. Here's what to expect and what you need to do before your situation gets worse.

What Happens Immediately After the Accident

You are personally liable for all damages from the accident — vehicle repairs, medical bills, property damage, and lost wages for everyone involved. Auto insurance covers these costs when a policy is active at the time of the accident. No policy means no coverage layer between you and the bills.

The other driver's insurance company will pursue you directly for reimbursement after they pay their policyholder's claim. This happens through demand letters first, then civil court if you don't pay. In most states, judgment amounts can lead to wage garnishment and asset liens. There is no statute of limitations reset once the claim enters court.

Your state's DMV typically receives an accident report within 10 days if police responded or if damages exceeded the state's reporting threshold — usually $1,000 to $2,500 depending on location. Once the DMV confirms you had no insurance at the time of the accident, they begin a separate penalty process that runs parallel to any civil liability.

State Penalties for Driving Uninsured After an At-Fault Accident

Most states impose an immediate license suspension once they verify you were uninsured during an at-fault accident. Suspension length ranges from 90 days to one year for a first offense, with longer periods for repeat violations. Some states add vehicle registration suspension, which means your car cannot be legally driven by anyone until you resolve the penalty.

Fines typically range from $500 to $5,000 depending on the state and the severity of the accident. States with mandatory insurance laws — 49 states plus the District of Columbia — treat uninsured driving as a separate violation from the accident itself. You can face penalties for both the accident and the lack of coverage simultaneously.

Reinstatement after suspension requires proof of current insurance, payment of all fines and fees, and in most cases, filing an SR-22 certificate with the state. The SR-22 is not a type of insurance — it is a form your insurance carrier files with your state's DMV proving you carry at least the minimum required liability coverage. Not all carriers offer SR-22 filing. You will need a company that works with high-risk drivers.

Find out exactly how long SR-22 is required in your state

Your Financial Liability Does Not Disappear When You Buy Insurance

Buying an insurance policy today does not cover an accident that happened yesterday. Auto insurance policies cover incidents that occur during the active policy period only. Retroactive coverage does not exist in standard or non-standard auto insurance.

You remain personally responsible for all damages from the uninsured accident regardless of when you secure future coverage. The other party's insurance company or the individuals involved can sue you in civil court to recover costs. Court judgments remain on your record and can affect credit, employment background checks, and future insurance eligibility.

Some states allow payment plans or settlement negotiations if you cannot pay the full amount immediately. Ignoring demand letters or court summons makes the situation worse — default judgments allow creditors to garnish wages without further negotiation.

How Much Insurance Will Cost After This

Drivers with an at-fault accident on record and a lapse in coverage typically see rate increases of 80% to 150% compared to standard rates. The uninsured status adds a separate surcharge on top of the accident penalty. If your state requires SR-22 filing, expect to pay an additional filing fee of $15 to $50, and the SR-22 designation itself signals high-risk status to insurers.

Non-standard auto insurance carriers specialize in covering drivers with violations, lapses, and accidents. Companies like Progressive, Dairyland, The General, Bristol West, and National General write policies for high-risk drivers when standard carriers decline coverage. Rates vary widely by state, age, and driving history, but monthly premiums typically range from $150 to $350 for minimum liability coverage with SR-22 filing.

SR-22 filing is usually required for three years after reinstatement, though some states mandate five years depending on the violation. During this period, any lapse in coverage — even one day — triggers a new suspension and restarts the SR-22 clock. Continuous coverage is the only way to complete the requirement and return to standard insurance eligibility.

Can You Negotiate or Settle the Damages

You can attempt to negotiate directly with the other driver or their insurance company before a lawsuit is filed. Some drivers accept structured payment plans to avoid court costs and attorney fees. Any agreement should be documented in writing and include a release of liability clause to prevent future claims on the same accident.

If the other party's insurer has already paid the claim under their policyholder's collision or uninsured motorist coverage, the insurer has subrogation rights — the legal right to recover what they paid by pursuing you. Subrogation claims are harder to negotiate because the insurance company has more resources and less incentive to settle for partial payment.

Bankruptcy can discharge some accident-related debts, but it does not remove the DMV suspension or eliminate the SR-22 requirement. Your license remains suspended until you meet your state's reinstatement conditions regardless of how the financial liability is resolved.

What To Do Right Now

Step 1: Contact a non-standard insurance carrier within 7 days to get a quote for SR-22 insurance if your state requires it for reinstatement. Even if your license is already suspended, you need an active policy in place before the DMV will process reinstatement. Waiting until after you pay fines wastes time — most states require proof of future insurance as part of reinstatement, not after.

Step 2: Request a copy of the accident report and your state's suspension notice within 10 days to confirm what penalties you face and what the reinstatement requirements are. Some states send notices to outdated addresses, and missing a deadline can add months to your suspension. If you haven't received anything within two weeks of the accident, contact your state DMV directly.

Step 3: Respond to any demand letters or court summons from the other driver or their insurer within the stated deadline — typically 20 to 30 days. Ignoring these does not make them go away. A default judgment allows the other party to garnish your wages and freeze bank accounts without further court proceedings. If you cannot pay the full amount, propose a payment plan in writing before the court date.

Step 4: Gather documentation of your current financial situation — pay stubs, bank statements, existing debts — if you plan to negotiate a settlement or payment plan. Courts and insurers are more likely to accept reduced settlements or extended payment terms if you can demonstrate genuine inability to pay in full immediately. Documentation also protects you if the case escalates to collections or judgment enforcement.

Step 5: Maintain continuous insurance coverage without any gaps once your policy begins. If you are required to file SR-22, a single missed payment that causes a lapse will trigger a new suspension notice sent to the DMV by your carrier. The SR-22 clock resets, and you start the three-year requirement over from the new reinstatement date. Set up automatic payments if your carrier allows it.